How To Set Up A Section 125 Cafeteria Plan

Why a Section 125 Cafeteria Plan is Worth the Piece of work for Employers

- Lauren Hargrave

- 4 min read

Get the details on Section 125 Plans and how they benefit employers looking to offer benefits like HSAs to employees.

There are many ways employers tin can provide benefits to employees and not all require a Section 125 Cafeteria Programme. But if an employer wants to enable employees to contribute office of their bacon to a qualified spending account like a Health Savings Account (HSA) or Flexible Spending Arrangement (FSA), and/or if the employer wants to make contributions to said employee accounts, they should maintain this document.

Information technology is possible for employers to make direct contributions to employees' accounts outside of a Section 125 Plan, but the rules that govern these types of contributions are strict and conduct a hefty penalization if they're not followed. Specifically, any contributions not made through a Sec 125 are subject to strict comparability rules. Employer contributions made through a Sec 125 plan are non subject to the comparability rules, but are subject to not-bigotry rules.

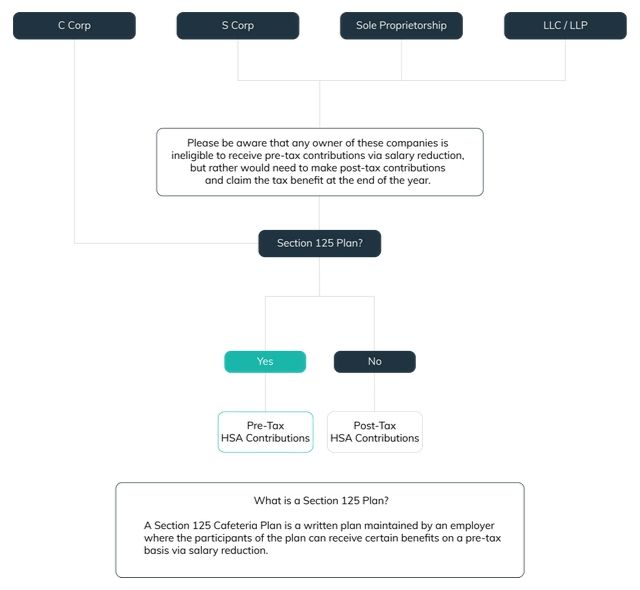

What is a Section 125 Program?

A Section 125 Cafeteria Programme is a written document maintained by an employer that outlines the rules which let employees to make tax-free contributions to qualified benefits accounts like HSAs. It must describe in item the benefits the cafeteria program offers, who is eligible to receive said benefits, and other rules about how the plan operates. It must include a taxable benefit (i.e. compensation) that'southward exchanged for a non-taxable do good (eastward.g. contributions to an HSA).

If the employer wants to contribute to employees' accounts, those contribution rules should be outlined in the cafeteria program besides. Employers can make straight contributions to employees' accounts without a cafeteria plan, merely if they cull to exercise this, they're required to requite every employee either the verbal same dollar amount or the same percentage of their health program deductible. If the employer doesn't follow this equitability rule, they could be subject field to a 35% tax.

Since a Section 125 Deli plan allows employers to fix their own rules for contributions (equally long as they don't run afoul of the anti-discrimination rules described later), it'due south a improve way for them to contribute to employees' accounts.

Rules for deli plans include:

Rule #1- Eligible benefits under a Section 125 Cafeteria Plan

An employer's cafeteria plan may encompass ane or multiple of the following benefits:

- HSAs

- FSAs

- Health Reimbursement Arrangements (HRAs)

- Dependent Reimbursement Account (DRA)

- Premium Simply Plans (POPs)

- Adoption Aid

- Blow and Health benefits (excluding Archer Medical Savings Accounts (MSAs) or long-term care)

- Group term life insurance

Rule #2- Who is eligible to receive benefits under a Section 125 Cafeteria Programme

The benefits described in the plan must be fabricated equally available to employees in the same situation, their spouses and dependents. Employers may also cull to include domestic partners and their dependents in those eligible to receive benefits.

The employer can choose to make rules about eligibility that relate to:

- Employee start engagement

- Employee participation (i.e. employee must elect to participate in the plan)

- Employee classification (east.g. role-time vs. full time)

- Employees under a commonage bargaining agreement

- Employee waiting periods

- Employees under age 25

- Foreign employees working abroad with no US income

- Geographic location/ rating area

- Special enrollment periods

- When individuals can modify their plan selections

- How individuals tin can finish plans

- Whatever combination of the above

The IRS prohibits discriminating against plan participants and beneficiaries based on health factors. That means a plan cannot restrict eligibility based on:

- Health factors (e.g. health condition, medical condition, disability, genetic information, etc.)

- Evidence of insurability (east.g. engaging in high-adventure adrenaline sports)

Dominion #3- Who can participate in a Section 125 Plan based on company type

- All eligible employees (as described in the plan document) of regular corporations, S-corporations, limited liability companies (LLCs), partnerships, sole proprietorships, professional person corporations and nonprofits.

- Anyone owning ii% or less of an Due south-corporation.

Dominion #four- Who is excluded from participating directly in a Section 125 Program based on visitor type

- Sole proprietorships: the Sole Proprietor.

- Partnerships: the partners.

- S-corporations: any private owning more than than two% of the company.

- LLCs: members.

How do these plans piece of work?

When an employee agrees to participate in the deli plan, they select the benefit(s) and the amount they wish to contribute, and so the employer subtracts the appropriate amount from each paycheck and deposits it into the selected business relationship(s).

How exercise the taxes work?

The general rule for Section 125 plans is: the contributions are tax-free. That means employees' contributions aren't subject to FICA, FUTA, Medicare tax or income tax withholding. Yet, our taxation code is complex and there are many forms of "taxes". And contributions to different benefit accounts are field of study to different tax rules. For the complete gear up of tax rules for different benefits accounts, refer to the IRS Employers' Tax Guide and Supplemental Tax Guide. Here are the basics:

- Contributions to group term life insurance policies that exceed $fifty,000 in coverage are bailiwick to: Social Security and Medicare taxes.

- Contributions to adoption assistance plans are subject to: Social Security, Medicare and FUTA taxes.

Employers also receive tax benefits from assuasive employees to access benefits through a Section 125 Plan. When employees make contributions to accounts like HSAs, employers don't pay the matching Social Security, Medicare and FUTA taxes on said contributions. Employers besides receive taxation breaks on contributions they make to employees' accounts on the employees' behalf.

If an employer offers a Section 125 Cafeteria Plan, there's no need for it to file additional paperwork with the IRS. The exception is if it offers a welfare program. If an employer offers a welfare plan, it may need to file a return for that program.

By setting up a Section 125 Cafeteria Plan, employers requite themselves the flexibility to offer benefits like HSAs and FSAs and set the eligibility and contribution rules that brand sense for their visitor. It also enables employers to reap greater tax benefits and support the health and well being of their workforce all at the same time.

Read more by Lauren Hargrave

Lauren Hargrave is a author from San Francisco who focuses on applied science, finance and wellness. She follows comedians like most people follow bands and believes an outdoor sweat session can cure almost any bad mood. She's also been writing her commencement novel for so long, her mom doesn't ask about it anymore.

Disclaimer: the content presented in this article are for informational purposes only, and is not, and must not exist considered tax, investment, legal, bookkeeping or financial planning advice, nor a recommendation every bit to a specific class of action. Investors should consult all available information, including fund prospectuses, and consult with appropriate taxation, investment, accounting, legal, and bookkeeping professionals, equally appropriate, before making whatever investment or utilizing any financial planning strategy.

Sign up for our newsletter

Stay up to date on the latest news delivered straight to your inbox

You're subscribed!

Expect a friendly hello in your inbox.

How To Set Up A Section 125 Cafeteria Plan,

Source: https://livelyme.com/blog/employer/section-125-plan/

Posted by: deciccobeirl1940.blogspot.com

0 Response to "How To Set Up A Section 125 Cafeteria Plan"

Post a Comment